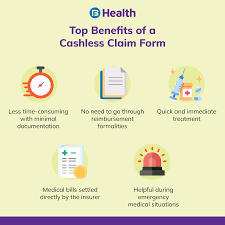

Cash Less

About The Term Insurance

Term insurance is a life insurance product, which offers financial coverage to the policyholder for a specific time period. In case of death of the insured individual during the policy term, the company pays the death benefit to the beneficiary. Individuals should consider Term Insurance as an Investment.

Benefits of Term Insurance:

- High Sum Assured at Affordable Premium – Term plan premiums are affordable and its very less compared to the Sum Insured provided

- Easy to Understand – Its simple and no complications are there so people can understand easily and mis-selling is less

- Additional Riders – Lot of additional riders are available at affordable rate and they are useful at stressful times

- Income Tax Benefits – Tax benefit is available under 80 C of the Income Tax Act 1961. The Insured can get a rebate of up to INR 1,50,000/- in a year on the premium paid. On top of this under section 10(10) D the final payout which is the sum Insured is exempt of tax in the hands of the beneficiary which plays a major roll as it helps people save tax and this can be considered as an Investment

- Critical Illness Coverage – More than 40 critical Illness are covered under the Term plan and one can take it as an add-on cover

- Accidental Death Benefit Coverage – This can also be taken as add-on cover. In case of death by accident the actual sum insured and additionally the accidental sum insured is also paid. For example, Base policy sum insured is INR 1 Cr and accidental death benefit is INR 1 cr, the beneficiary gets INR 2 cr and in few policy if the accident happens in mass transit like bus, train or flight then the accidental death benefit becomes double and the beneficiary gets INR 3 Cr.

- Return of Premium Option – Few Insurers offer this option, but one should be careful as the premium is higher than the normal term policy

Disadvantage of Term Insurance:

- Surrender Value – The Insured can stop paying the premium at any point of time and the policy will become null and void. The Insured will not get any benefits from the policy all the payment done will go for waste. The Surrender value will vary with policy depending on the terms of the policy

- No Maturity benefit – Lot of life Insurance policy offer maturity benefits, bonuses and more but term Insurance doesn’t offer any of these. It acts as a proper Insurance and covers only the life

- Premium goes up with age – The earlier you take the policy premium is less as your age goes up the premium also goes up. Premium also goes up depending on the pre-existing dieses and medical test repot

Requirements:

Age: Insurance companies often have age restrictions for purchasing ROP term policies. The policyholder usually needs to fall within a specific age range, which can vary between providers.

Health Status: The applicant may be required to undergo a medical examination or provide health information to determine eligibility. Some ROP policies may have stricter health requirements compared to traditional term insurance.

Financial Stability: Insurance companies may assess the financial stability of the applicant to ensure they can afford the premiums throughout the term of the policy.

Smoking Status: Tobacco use can significantly affect premiums. Applicants are typically asked about their smoking habits, and smokers may face higher premium rates.

Coverage Amount: The amount of coverage (death benefit) desired by the applicant may impact eligibility. Insurance companies may have minimum and maximum coverage limits.

Policy Term: ROP term policies are available for specific terms (e.g., 10, 15, 20 years). The applicant needs to choose a term that aligns with their needs and eligibility criteria.

Premium Payment Capability: The applicant needs to demonstrate the ability to pay the higher premiums associated with ROP term policies. These premiums are usually higher than those of traditional term insurance.

No Serious Medical Conditions: Applicants with serious pre-existing medical conditions may face challenges in obtaining ROP term insurance or may be subject to higher premiums.

Underwriting Approval: The insurance company's underwriting process assesses the applicant's risk profile. Approval is based on factors such as health, lifestyle, and other underwriting criteria.

It's important to note that meeting these basic requirements does not guarantee approval, and the specific terms, conditions, and eligibility criteria can vary among insurance providers. Individuals interested in purchasing a Return of Premium term policy should consult with insurance professionals, carefully review policy details, and compare offerings from different companies to find the best fit for their needs.

Disclaimer:

A disclaimer for Return of Premium (ROP) term insurance would typically include information to clarify the terms and conditions of the policy. While the language may vary, here are some elements that might be included:

Premium Refund Conditions: Clearly outline the circumstances under which the policyholder is eligible for a premium refund, emphasizing the requirement for the insured to survive the entire term of the policy.

Premium Amounts and Payment Terms: Specify the premium amounts and the schedule of payments, including any potential changes over the term of the policy.

Investment Component: If applicable, explain how the investment or savings component of the policy works, highlighting any potential risks or limitations.

Death Benefit Conditions: Clearly state the conditions under which the death benefit will be paid to beneficiaries, emphasizing the distinction between the death benefit and the premium refund.

Policy Renewal: Provide information about the terms for policy renewal, if applicable, including any changes in premiums, coverage, or conditions that may occur at renewal.

Exclusions and Limitations: Clearly list any exclusions or limitations that may apply to the policy, such as specific events or circumstances that may not be covered.

Cancellation and Surrender Terms: Explain the conditions and consequences of policy cancellation or surrender, including any fees or penalties that may apply.

Financial Disclaimer: Include a disclaimer stating that the policy is not an investment and that the return of premiums is contingent on the insured surviving the entire term.

Legal Disclaimer: Include a legal disclaimer stating that the document is not a contract and that the terms and conditions are subject to change, with the actual insurance policy being the legally binding agreement.

It's crucial for policyholders to carefully read and understand the disclaimer and the entire insurance policy to ensure they have a clear understanding of the coverage, potential returns, and any associated terms and conditions. If necessary, seeking professional advice is advisable.

Covered In Insurance

Lorem ipsum dolor sit amet, consectetur cing elit. Suspe ndisse suscipit sagittis leo sit met um dolor sit amecond imentum esti

Who Will Covered You?

Frequently Asked Questions

Our friendly customer support team is your extended family. Speak your heart out. They listen with undivided attention to resolve your concerns. Give us a call, request a callback or drop us an email, we’re here to help.