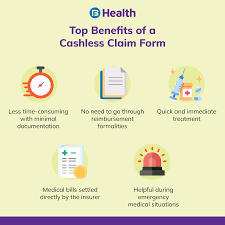

Cash Less

Return of Premium Term Insurance

About The Return of Premium Term

Return of Premium (ROP) term insurance is a type of life insurance that combines the features of traditional term life insurance with a savings or investment component. With a regular term life insurance policy, if the insured person survives the policy term, there is no payout, and the premiums paid are essentially the cost of insurance.

In contrast, Return of Premium term insurance offers a refund of the total premiums paid by the policyholder if they outlive the policy term. Here's how it generally works:

Premium Payments: The policyholder pays regular premiums throughout the term of the policy, typically ranging from 10 to 30 years.

Survival Benefit: If the insured person survives the entire term of the policy, the insurance company refunds all the premiums paid during that period.

Death Benefit: If the insured dies during the term, the beneficiaries receive the death benefit as with traditional term life insurance.

Advantages of Return of Premium (ROP) Term Insurance:

Premium Refund: The primary advantage is that if the policyholder outlives the term, they receive a refund of all the premiums paid, providing a financial return on their investment.

Financial Security: Like traditional term insurance, ROP term insurance provides a death benefit to beneficiaries if the insured person passes away during the policy term, offering financial security for the family.

No Loss of Premiums: Unlike regular term insurance where premiums are not refunded if the policyholder survives, ROP ensures that money is not "lost" if the insured outlives the policy.

Disadvantages of Return of Premium Term Insurance:

Higher Premiums: ROP term insurance typically has higher premiums compared to standard term insurance. This is because it includes the cost of insurance plus the savings component for the premium refund.

Opportunity Cost: The higher premiums of ROP could potentially be invested elsewhere for potentially higher returns. Critics argue that the investment component of ROP may not yield as much as other investment options.

Complexity: ROP policies can be more complex than traditional term life insurance. Understanding the terms and conditions, as well as the potential benefits and drawbacks, requires careful consideration.

Delayed Return: The return of premiums occurs at the end of the policy term, so policyholders won't see a return until they've paid premiums for the entire term. This means that the return may be subject to inflation, reducing its real value.

When deciding between ROP term insurance and traditional term insurance, individuals should assess their financial goals, risk tolerance, and consider whether the potential return of premiums justifies the higher cost of premiums associated with ROP. It's advisable to carefully review and understand the terms of the policy before making a decision.

Requirements:

Age: Insurance companies often have age restrictions for purchasing ROP term policies. The policyholder usually needs to fall within a specific age range, which can vary between providers.

Health Status: The applicant may be required to undergo a medical examination or provide health information to determine eligibility. Some ROP policies may have stricter health requirements compared to traditional term insurance.

Financial Stability: Insurance companies may assess the financial stability of the applicant to ensure they can afford the premiums throughout the term of the policy.

Smoking Status: Tobacco use can significantly affect premiums. Applicants are typically asked about their smoking habits, and smokers may face higher premium rates.

Coverage Amount: The amount of coverage (death benefit) desired by the applicant may impact eligibility. Insurance companies may have minimum and maximum coverage limits.

Policy Term: ROP term policies are available for specific terms (e.g., 10, 15, 20 years). The applicant needs to choose a term that aligns with their needs and eligibility criteria.

Premium Payment Capability: The applicant needs to demonstrate the ability to pay the higher premiums associated with ROP term policies. These premiums are usually higher than those of traditional term insurance.

No Serious Medical Conditions: Applicants with serious pre-existing medical conditions may face challenges in obtaining ROP term insurance or may be subject to higher premiums.

Underwriting Approval: The insurance company's underwriting process assesses the applicant's risk profile. Approval is based on factors such as health, lifestyle, and other underwriting criteria.

It's important to note that meeting these basic requirements does not guarantee approval, and the specific terms, conditions, and eligibility criteria can vary among insurance providers. Individuals interested in purchasing a Return of Premium term policy should consult with insurance professionals, carefully review policy details, and compare offerings from different companies to find the best fit for their needs.

Covered In Insurance

Lorem ipsum dolor sit amet, consectetur cing elit. Suspe ndisse suscipit sagittis leo sit met um dolor sit amecond imentum esti

Who Will Covered You?

Frequently Asked Questions

Our friendly customer support team is your extended family. Speak your heart out. They listen with undivided attention to resolve your concerns. Give us a call, request a callback or drop us an email, we’re here to help.